Student living: keeping your money safe

Avoiding scams and ensuring your finances are secure are both important lessons for student life. Tom Allingham, Head of Editorial at Save the Student, explains how to stay safe financially.

Taking the leap into university life can be tough, which is why MoneySense has created this series of articles to help your teen adjust to and build confidence in their independent life. Why not share this with them?

You might think that getting scammed online is nothing to worry about – that it’s the kind of thing that would only happen to an older relative, or someone who doesn’t understand technology. And, in a way, you’d be right: these groups are among the most vulnerable to scams.

But the truth is that anyone can fall victim to a scam, and nowadays there are all kinds of schemes out there specifically targeting young people. Obviously, these are illegal, but spotting them can be tricky, especially when you find what you think is an incredible bargain or a tonne of money.

So, let’s take a look at some of the most common scams, how to avoid them and why you should never get involved.

Common types of scam

There are dozens, if not hundreds, of types of scam, but let’s just focus on some of the ones you’re most likely to face:

- Phishing, smishing and vishing: Phishing is when scammers send out emails that are designed to trick you into revealing valuable information such as account details and passwords, or tempting you to click on unsafe links. Emails often pretend to be from banks, well known brands or even the tax office, and fraudsters copy official designs and logos to catch you off-guard. ‘Smishing’ is the SMS or text message equivalent of phishing, and ‘vishing’ is short for ‘voice phishing’, where you receive a phone call and fraudsters try to convince you to share personal or financial information. Cases of smishing and vishing have gone up dramatically, so stay alert.

- Malware and spyware: Be careful what you download, because spyware and malware are often disguised as software or apps. Installing them on your computer or phone could seriously damage your device and put your personal information at risk.

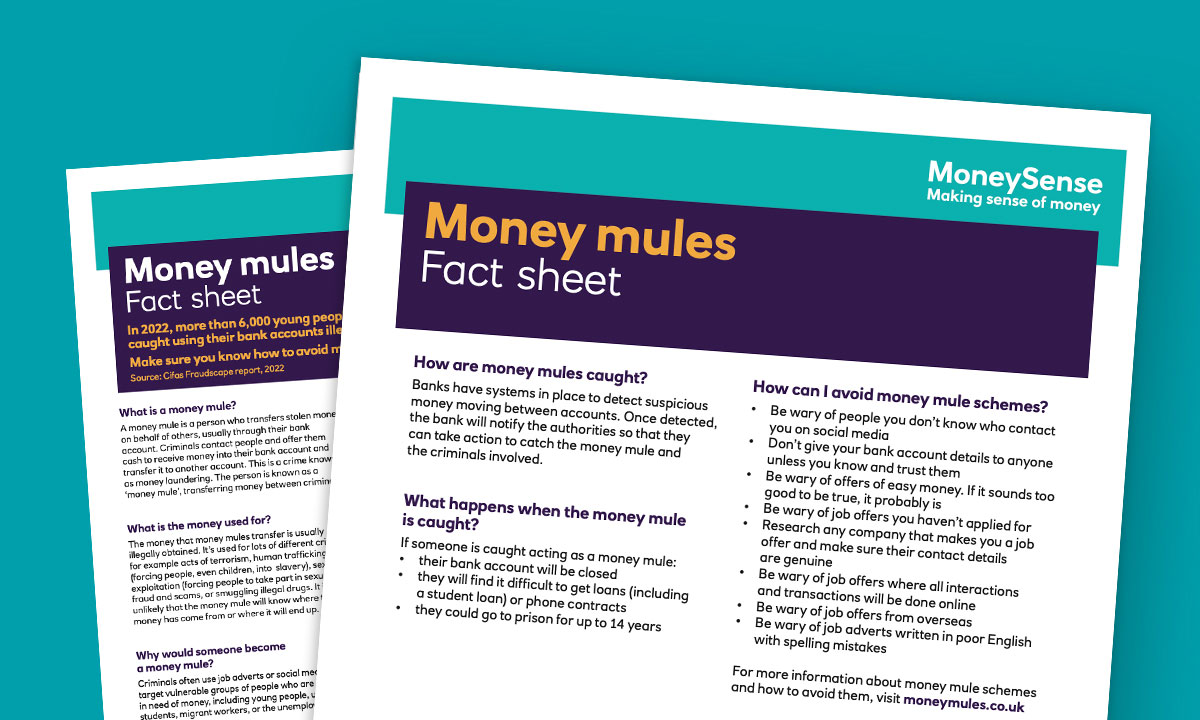

- Money muling: If you’ve ever watched Breaking Bad or Ozark, you’ll know that criminals often need to hide (or ‘launder’) their money to avoid the authorities. In this instance, they’ll contact someone (the ‘mule’) and ask if they can temporarily transfer money into their account. In return, the mule is promised a cut of the money, which has often been earned from illegal activity.

- Fake websites and products: Can’t believe a new iPad is available for £150, or that you can get two tickets to a popular festival for the price of one? Chances are, the website (or, at the very least, the product being sold) is a total scam, and you’ll never see your money, or what you paid for, ever again.

The consequences of scamming

Clearly, getting scammed can mean you spend money without getting anything in return. But if the scammers get hold of your login details or other personal information, they could then gain access to all kinds of other accounts in your name – especially if you use the same passwords across the board.

What’s more, if you became involved in money muling, you could end up with a criminal record. The number of young people being recruited as mules has risen massively in the last few years, with fraud prevention body Cifas reporting a 78% increase in under 21s taking part in money mule activity in 2021 compared to 2020. Even though you’re just the ‘middle man’ in the laundering process, you’re liable for the crime too. If caught, you could face a prison sentence and find it difficult to borrow money in the future. And even if you’re not caught, it’s worth thinking about where that money has come from. It’s being kept secret for a reason, be it to avoid tax or to hide the fact that the scammer is profiting from illegal activity, such as drug dealing or human trafficking. Take a second to consider whether you want to be involved in this, especially as mules who agree and later try to quit can be threatened with violence.

How to avoid being scammed

This sounds like scary stuff, but fortunately there are some really easy steps you can take to avoid falling victim to a scam:

- Check for https: Before entering any personal or payment details, always look at the URL in the address bar. If the address says ‘http’ at the start rather than ‘https’, the website isn’t secure and your information could be at risk.

- Research companies: Never heard of the company you’re about to shop with? Do a quick search for their name plus ‘reviews’, and sites like TrustPilot will be able to give you a good indication of whether or not they’re the real deal.

- Only respond to official communication: Your bank has a few red-lines it will never cross, like asking for your full PIN or online password via phone or email. Check the email or phone number they’ve contacted you from and, if in doubt, call your bank using the number listed on your card to ensure you’re speaking to somebody official – even if it means hanging up on a possible fraudster.

- Update antivirus software: We’re all guilty of clicking ‘not now’ when prompted to update, but do this too often and you may as well be posting your personal details on your social media accounts. Hackers are always developing new ways to access people’s information, but antivirus software is never too far behind – so keep it updated.

- Use a password manager: Having the same password for all of your accounts is a scammer’s dream, but how else are you meant to remember 27 different sets of login details? Well, with a password manager. Services like LastPass or 1Password offer a secure virtual-vault to store your details – as well as other neat features like help with pre-filling forms and generating passwords.

Image credits: iStock

Find out about all the latest MoneySense articles for parents by following us on Facebook

Related activities

Want your teenager to find out more for themselves? Here are some activities to share with them.

Articles:

Articles:

Information:

Information: